Getting the job you’ve always wanted in another country is the beginning of a new adventure in life where you will encounter new challenges and have plenty of room for personal growth, especially financially. As you move on to this new chapter, managing your financial aspect in India is something that you should look at. A critical element of this is to shift fund transfer NRO to NRE Account, which is a must for NRIs; doing this ensures a smooth financial transition from the home country. In the upcoming article, we will go a step further and learn about the easy but essential ways of transferring the money you have worked hard for between the global and Indian financial accounts and keep your money management flowing smoothly.

RBI Guidelines about Fund Transfer NRO to NRE Account

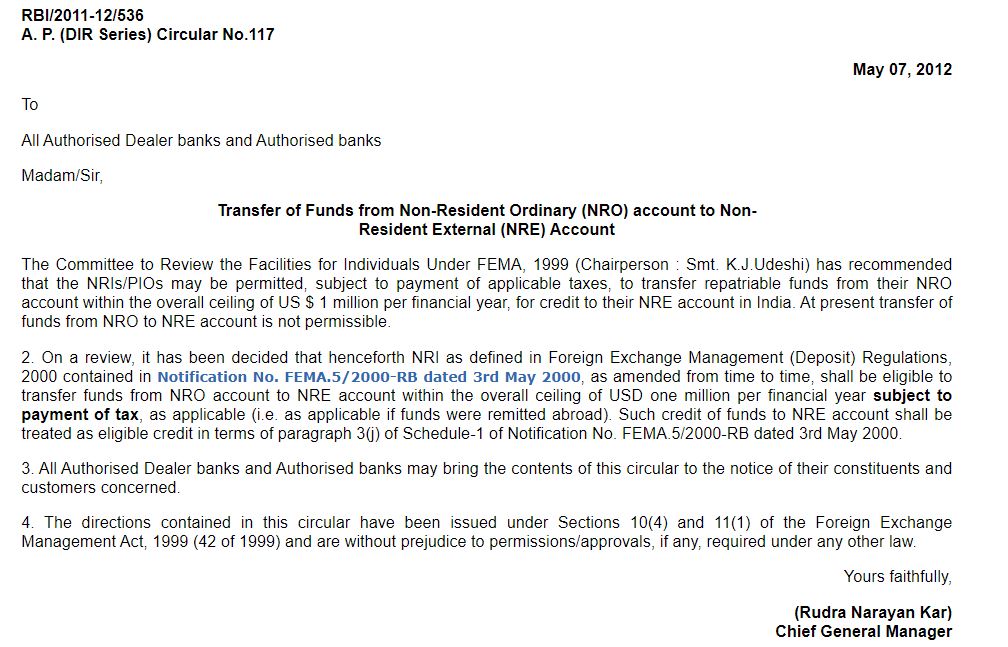

As per the Reserve Bank of India dated May 7, 2012 notification, “ It has been decided that henceforth Non-resident Indians as defined by Foreign Exchange Management (Deposit) Regulations, 2000, notified in notification number…” Incoming Remittances (Non Resident Ordinary, i.e. NRO) account shall be entitled to transfer fund transfer NRO to NRE accounts within the overall ceiling of USD one million per financial year subject to payment of such tax, if any (i.e. as applicable if NRO funds were remitted abroad). A credit of funds to NRE account will be considered as an eligible credit as per sub-par (3)(j) of Schedule-1 of Notification no. FEMA Notification 2000 B dated 3rd May, 2000 5 (R.B).” Please see the document as attached to Know more.

RBI before had put a limit on the money that can go from an NRO account to an NRE account. Receiving such amount from a foreigner or from existing NRE account was the single way to get money into NRE accounts.

There could be some cases where you have to do a transfer of funds into an NRE account. Trading again in Indian rupees you might need to transfer and withdraw in your favour currency the money you’ve earned in Indian rupees. One may need to have an NRO account only for the purpose of collecting Indian revenue. Then, keep all your investments in the NRE account and if/ when you need the money, you can have the flexibility of complete repatriation.

The Reserve Bank of India (RBI) has specifically mentioned the directives for the transfer fund transfer NRO to NRE account.

Here are the key points related to Fund Transfer NRO to NRE Account as per RBI guidelines:

- Quantum of transfer: The limit for such a transfer fund transfer NRO to NRE account is that of USD1 million per annum.

- Tax compliance: The amount that shall be transferred shall be subject to remittance and should have no tax liabilities. This means that any applicable taxes on the funds attributed to the NRO Account should be paid in full before their transfer.

- Form 15CA and 15CB: This is the list of those Indian Income Tax department’s certificates which are compulsory. (C) Form 15CA is a statement by the remitter that the tax has been deducted on the funds and Form 15CY is a certificate by a Chartered Accountant attesting to the same.

Required documentation:

While thinking through the procedure of sending money to an NRE account, it is crucial to get the required papers to make the process of fund transfer NRO to NRE accounts smooth and compliant.

- Form 15CA and 15CB: What has been said earlier, these are the most important notice for tax compliance.

- Bank forms: Special modifications or statements that your bank requires.

- Identity and address proof: Valid passport, OCI/PIO card or address proof – both Indian and overseas.

- Bank statements: Statements of the NRO Accounts as evidence of source of funds.

(NRO = Non Resident Ordinary Citizen) - Other supporting documents: On the basis of the source of money (receipt, dividends, etc.), applicable documents may be required.

Purposes for the transferring funds from a NRO Account to a NRE Account

Apart from the above-discussed advantages, there also exist some other strong reasons for an NRI to go for an NRO to NRE transfer online.

Mostly, the choice is found in the fact that an NRE Account has more flexibility and advantages than an NRO Account.

FAQ’s

What is an NRO Account?

The NRO (Non-Resident Ordinary) account is meant for a Non-Resident Indian (NRIs) to carry out their operations with their income earned in India. This could be rents, dividends and even pensions. The salient feature of an NRO account is that it can accommodate funds in Indian rupees (INR). Nevertheless, such repatriation of money from those accounts is within the limits and under the condition of certain regulations.

What is an NRE Account?

While a resident account is suitable for an NRI who wishes to transfer his earnings sent from abroad, an NRE account is the perfect choice for an NRI who wants to park his foreign earnings in India. The major advantage of an NRE Account is that all the amounts, including both the principal and interest earnings, are transferable out of the country. Also, the income generated from NRE Accounts is not taxed in India, making it an attractive option for NRIs.

Transfer between NRO and NRE accounts is possible?

Yes, you can transfer money from your NRO account to the NRE account. In addition to the transfer, money can also be transferred from an NRE account to another NRE account. However, do not forget that you cannot transfer funds from your savings account in India to an NRI account.

Can I have both the NRE and the NRO account at one time?

An NRI’s account is required to be of type Non-Resident External (NRE) or Non-Resident Ordinary (NRO), in order to transact anything in India. However, a NRI/PIO client can choose to open any of the two account types cited above depending upon specific transactional needs, e.g. NRE and NRO Accounts, or even both.

Which savings account is more profitable NRE or NRO?

One has to go for NRE account if he desired to park or maintain his foreign earnings in Indian Rupees. NRE Accounts are also favoured if one wishes to keep the savings liquid. Choose NRO accounts if you need to put your income from India in Indian currency.

What are the disadvantages of NRO bank accounts?

The scope of repatriation activity is restricted for NRO accounts. The NRO account forbids you to make more than USD 1 million net of taxes in one assessment year. The amount of interests can be remitted without any restrictions, but the principle can be repatriated only up to the fixed amount.

Who is NRE account eligibility?

Opening the NRE account is possible only with a NRI personally and not by the Power of Attorney Holder. A Naturalized Resident (NRI) can have multiple NRE accounts in India. NRE account/s can be opened jointly with other NRIs; however, it cannot be opened with any resident.

Am I eligible for 2 Non-Resident accounts?

Yes, you are also allowed to open and operate with more than one A/C’s

Is PAN number required in NRE?

An NRI is mandatorily required to possess a PAN card in the following scenarios:

Assuming an NRI earns a taxable income in India.

If an NRI wants to buy and sell share say through depository or through broker.

If he\she would like to invest in a Mutual Fund.

Can my friend transfer money to my NRE Rupee account?

Rupee-funded transfers in local transactions in Indian NRE Accounts are not allowed.

You can only technically send fund in the NRE account, in that case in which the money is converted from the foreign currency into INR.

Is the NRO Account to NRE transfer allowed?

Transfer of funds from an NRO Account to a NRE Account is permissible, however, it has to be subject to rules put forward by the Reserve Bank of India (RBI).

Understanding these guidelines, the process, and the documentation therefore is a very important for a seamless handover.

The maximum limit for fund transfer NRO to NRE accounts

The Reserve Bank of India has given the permission for the transfer of up to USD 1 million every year from an NRO to an NRE account.

Disclaimer:

The information contained in this article is general in nature and for informational purposes only. It does not serve as a replacement for advice that is specific to your circumstance.

The purpose of this article on “Fund Transfer NRO to NRE Account – Complete Guide” is to give general advice on the way funds are transferred from Non-Resident Ordinary (NRO) accounts to Non-Resident External (NRE) accounts in accordance with the RBI rules. All the attempts have been made to ensure the correctness of the data but it is advised to readers to discuss the specific advice with financial as well as legal professional accordingly.

The RBI mentioned in this article can change their guidelines any time and which make the readers to periodically verify the latest regulations before the fund transfer transactions. the paper looks at different aspects thereof, such as the quantum of transfer, tax filing, the necessary documentation and the purpose of remitting funds. Nonetheless, it should be mentioned that every case is unique, and the article may not be able to cover all possible situations.

The readers must get the required documentation and follow the regulations that are currently in effect whenever they engage in any fund transfer activities between NRO and NRE accounts. The article is focused on shedding light on the advantages and differences between NRO & NRE accounts, criteria for eligibility, and general information. Readers are advised to carry out comprehensive research and consult the professionals to have the right decision, which is suitable for them in particular.

The article is merely intended as a general guideline and does not constitute a complete solution to each individual’s financial issue. Readers are therefore advised to exercise the utmost care and get the requisite expert guidance. Neither the author nor the publisher will be held liable for any consequences arising from the operation or non-operation of the ideas in this article.